A sustained US$100 / bbl oil price could unlock up to 2.1mn bpd of additional crude supply across South America by the mid-2030s, according to new analysis by Rystad Energy

A sustained US$100 / bbl oil price could unlock up to 2.1mn bpd of additional crude supply across South America by the mid-2030s, according to new analysis by Rystad Energy

Global oil supply plummeted by 10.1 mn bpd to 97 mn bpd in March, according to the IEA, with continued attacks on energy infrastructure in the Middle East and ongoing restrictions to tanker movements through the Strait of Hormuz sparking the largest energy crisis in history. The supply situation looks unlikely to be resolved any time soon. Even once the Strait of Hormuz re-opens, it will still take some time to re-establish oil flows and restore lost Middle East production.

“The Middle East conflict has done more than spike oil prices — it has exposed how dangerously concentrated global supply chains are around the Strait of Hormuz. South America is now positioned as the world’s most consequential source of incremental supply. The region offers scale, geologic quality and relative political stability at exactly the moment that the world is shopping for alternatives,” said Radhika Bansal, Senior Vice President, Oil & Gas Research, Rystad Energy.

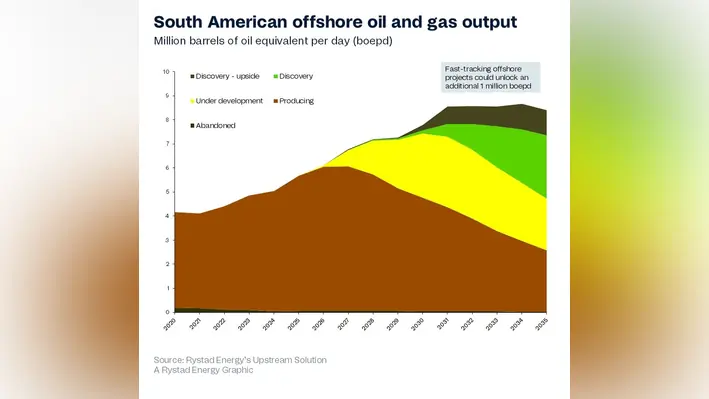

Offshore developments in Brazil, Guyana and Suriname represent the most immediate source of upside, says Rystad. Fast-tracking projects across these markets could deliver more than 1mn barrels of oil equivalent per day (boepd) of additional production over the next decade, backed by around US$33bn in incremental greenfield capex through 2035. In Guyana, ExxonMobil is targeting up to 300,000 bpd from its Yellowtail project, which came online at an initial average production of 250,000 bpd, and Rystad believes debottlenecking could unlock an additional 80,000 to 90,000 bpd across the Errea Wittu, Jaguar and Hammerhead fields. However, limited shipyard capacity for new FPSOs remains a constraint.

In a high-price scenario, Rystad Energy estimates Venezuela, which has now re-entered the global market, could add 910,000 bpd by 2035, with majors such as ExxonMobil and Shell assessing opportunities and signing preliminary agreements, although progress will depend on sanctions relief and fiscal reform. Production could grow even more if more players come in as investor confidence improves. Increased participation in underdeveloped fields, particularly through partnerships with PDVSA, the state-owned oil and gas company, would further unlock additional production potential, Rystad comments.

As for Argentina’s Vaca Muerta, crude production, currently around 600,000 bpd, could reach as much as 1.5mn bpd in 2035 in a high price scenario, says Rystad.

“The pace of growth across South America will depend less on resource availability or economics and more on execution capacity, supply-chain constraints and the broader investment environment. Countries that provide clear fiscal and regulatory frameworks are better positioned to accelerate project sanctions and capture the upside from higher prices. Those that hesitate or are slow to move will simply watch the capital flow elsewhere,” Bansal added.